Delta Wealth Solutions Strategy Lab

Welcome to the Strategy Lab. The Delta Wealth Solutions Strategy Lab focuses on providing the necessary insights to help clients achieve optimal investment and planning outcomes. Please check back regularly for our quarterly market newsletter along with commentary on the stories that move markets.

July 2026

Delta Strategy Lab - Market Update

250 Years of America & Compound Interest

In an extended celebration of the 250th anniversary of the US Declaration of Independence, Delta Wealth Solutions would like to take a quick moment to review one of the country's most beloved Founding Fathers, Benjamin Franklin. Old Ben was a key piece to the entire revolution, spanning from his time as a colonial businessman and civic leader, to his time as US representative to France during the war, and culminating in his oversight at the Constitutional Convention. What most don’t fully understand is that Franklin was also a keen investor in his day, amassing a large net worth that was never able to be fully quantifiable. One investment Franklin made was endowing 1,000 pounds sterling upon his death to the cities of Boston and Philadelphia, with strict stipulations for its investment and subsequent usage over the next 200 years. These endowed funds have been used to fund pubic works, scholarships for apprentice tradesmen, building projects, educational grants, and the establishment of the Benjamin Franklin Institute of Technology. Due to the unique distributions of the funds at the 100 and 200 year marks, the exact math of the total dollar value of the investment is still debated, but most agree it to be well in excess of $10,000,000 US dollars. How impressive! Franklins foresight to the growth of our nation and investment in that growth paved the way for a significant sum to be left largely for the betterment of its society and education of its young people. Today, we believe Franklin would be astounded at the ability of individual investors to access capital markets and grow their wealth. The US has become the beacon of trade and commerce throughout the world and its public equity markets are open for anyone to purchase stock. With access to such markets, and a proper long term time horizon (even if not 200 years!) then success remains available to todays investors as well.

Where do I stand with my financial plan?

Continuing with a focus on Benjamin Franklin, let’s review a couple of quotes from his Poor Richard’s Almanack. First, “No gains without pains.” from the 1745 publication. Investors understand that markets follow a random walk and pain can come with that from time to time. Recent examples include the 2022 inflation rise, 2025 tariff announcement, or this years war in Iran. In all examples pain was felt by investors yet, with a proper strategy, gains followed. Fast forward a couple years when Franklin says, “Lost time is never found again.” in the 1947 publication. How true this is for investors as well. A proper plan is extremely important, and keeping time horizon to the forefront remains key for long term success. Finally, in his The Way to Wealth essay, Franklin says, “An investment in knowledge pays the best interest.” Investors would be wise to take investment knowledge gathered over the past decades and conclude that utilizing sound strategy is better than attempting to find the next hot stock or get rich quick scheme. In conclusion, Franklin saw the benefit in using open markets and proven long term investment principles such as diversification to create wealth, and Delta Wealth Solutions aims to do the same for its clients.

"Don't worry about the world coming to an end today. It is already tomorrow in Australia." Charles Schulz

America's 250th Starts with a Boom

America’s 250th started off with a boom. That’s metaphorical for US strikes on Iran as well as global markets. At the end of the first quarter large-cap growth stocks were down nearly 10%, the S&P 500 was down 5% and other market segments had only squeaked out minor gains. Fast forward to the end of June and every market segment (see Callan chart on pg. 5) was positive. Small caps are leading the chart for the first time in over 10 years. With the Delta Wealth Solutions preferred small-cap ETF, (Avantis Small Cap Value AVUV) up 23% year-to-date. Another pleasant surprise was the firms preferred real estate ETF, (iShares US REIT) appreciated 21% year-to-date. Diversification for the first time in a number of years is finally working out to the benefit of US investors. Furthermore, fixed income was able to generate positive returns on the year even though interest rates, as measured by the US 10-year treasury yield, have risen 0.25%. Higher coupon payments across the yield curve are insulating investors from some interest rate volatility.

Though it has been a banner first half of the year, investors should remain cognizant of the risks on the horizon. While war in Iran has quieted down, a memorandum of understanding doesn’t mean it’s over. Mid-term election years quite often experience market volatility going into November. We wouldn’t be surprised if this year was similar. Generally incumbent presidents lose the house in mid-term election years, and occasionally the Senate; however, this year Gerrymandering by both parties in their respective states have made the margins for majority much slimmer. Over the coming days Delta Wealth Solutions plans to rebalance client portfolios that are out of balance, not because we aren’t optimistic on America’s future, because we are. Simply because of the old saying, “Bulls make money, bears make money, pigs get slaughtered.” No one has gone broke taking a profit, and we don’t intend to miss this opportunity either.

Technology Valuations have Reset

If one has read our newsletters before or sat through a meeting with one of our wealth managers it’s likely they have heard earnings generally drive stock market returns over the long-term. Our industry often utilizes what is called the “Forward Price to Earnings Ratio” or Forward P/E. Over short time frames this ratio fluctuates high and low through periods of greed and fear while over longer time frames valuations migrate to towards their average. In newsletters and discussions over the past few years we had expressed concern about AI and it’s impact on euphoric stock valuations. In our view, one of two things would happen—these companies would grow into their sky high valuations or the bubble would burst and prices would come down. In the tech sector specifically, a bit of both has occurred. According to JP Morgan Analyst Estimates, the technology sector is expected to grow its earnings by ~40% over the next twelve months1. At the same time the Roundhill Mag 7 ETF (MAGS) is down ~2% as of this writing. If you believe the earnings projections, which we do, it has created the phenomenon where the Technology Sector is trading at a similar valuation to last years tariff tantrum. Furthermore, the technology sector is now trading at lower valuations than the broad based S&P 500 index which hasn’t happened in recent history. In our view, this is an opportunity for investors to reallocate incrementally to technology and more broadly the growth area of the market.

Sources: Duality Research - dualityresearch.substack.com 4 July 2026

US Corporate Profit Engine Continues to Run

Similar to how profit growth is critical in the technology sector, it is just as consequential across the broad market. According to the CFA Institute and Robert Schiller’s data analysis, over the long term, using a data series from 1871-2024 the correlation between stock prices and earnings sits at 98%. In simple terms, 98% of the variation in stock prices can be explained by what is going on with corporate profits2! Zooming into today, corporate profits continue reach new all-time highs and according to analyst estimates this growth should continue for the foreseeable future. Coming into the year, analysts polled by JP Morgan were expecting ~12-13% earnings growth for S&P 500 companies. As of the end of the 2nd quarter, 2026 earnings estimates sit near 24%3. When corporate profits are accelerating it shouldn’t come to anyone’s surprise the market has seen new all-time highs this year. Even with the headwinds of War in Iran, higher interest rates, and mid-terms, in our view, this won’t be enough to stop the momentum of corporate America in the short-term, and in turn, that should be a positive for stock prices.

Source: Carson Investment Research @sonusvarghese via X formerly twitter

Changes in AI Happen Fast

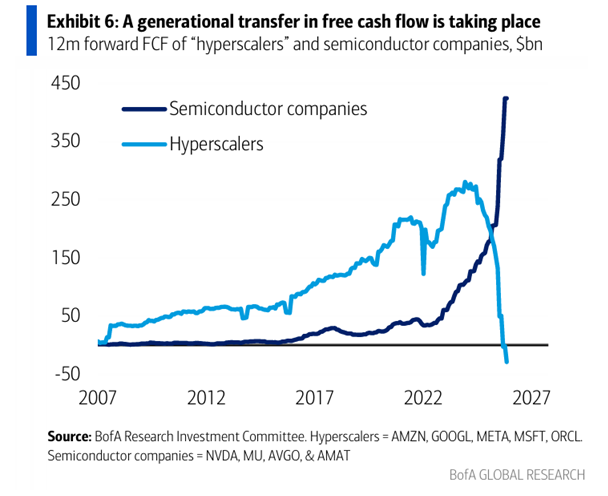

More and more in client conversations we are fielding questions about how best to position to take advantage of AI. Often it’s a question about this stock or that stock. In our view, it’s easy to see what has performed great over the last 5 years. It’s a much more difficult challenge to select what is going to significantly outperform over the next five years. When Microsoft initially expanded its partnership in OpenAI in January 2023, the “Hyperscaler” sector saw its stocks rally higher in anticipation of future AI payoffs. Hyperscalers are cloud service providers that offer on-demand computing power and storage globally. Companies such as Microsoft, Google, Amazon, and Oracle saw their stocks rocket higher in anticipation of outsized profit growth.

Fast forward to 2026, the Hyperscalers are seeing their free cash flow plummet as expenses and buildout continue to come in higher than initially projected4. As a result semiconductor companies such as Micron, Intel, and Applied Materials (Note: a company’s reference is not a recommendation to buy or sell a security) are seeing their profits and stocks rise exponentially while the Hyperscalers are seeing their stocks fall 25-50%. In the software industry, the concern about AI taking over is becoming so dire many analysts are now coining the phrase “SaaSpocalypse” short for Software as a Service Apocalypse. Delta Wealth Solutions continues to believe a broad exposure approach to all things AI is the optimal way to gain responsible exposure to the AI trend. DWS preferred holdings SPYG and QGRO have broad based exposure to all market segments involved in the AI buildout. In our view, this way is optimal because you don’t have to select the individual winners and losers, as long as the secular trend remains intact investors should benefit.

Don't Mix Politics and Investing

We are nearing the part of the political cycle where every two years it is worth reminding investors that while elections have material policy impacts, they generally don’t have long-term market impacts. Going into the mid-term elections, emotions will run high and we would encourage investors to not let their feelings about either party dictate their portfolio positioning. Regardless of political outcome, Delta Wealth Solutions will not make emotional portfolio policy decisions on our managed portfolios. Mathematically, a divided house and senate is highest probability outcome. Republican’s majority in the house is already razor thin due to retirements. According to Grok, since 1950 the incumbent president’s party lost seats in the house 89% of the time5. The only two presidents to buck the trend were Clinton in 1998 and Bush in 2002. No matter what happens in the mid-terms, we expect the balance of power to be slim either way, not materially different than it is now. The last two years of president Trump’s term will likely be dictated by executive action and very few pieces of completed legislation. Lastly, whether the home team wins or loses there is a high probability ones diversified investment portfolio will continue to achieve positive returns. The chart below details Democrat administrations in blue, and Republican administrations in red. In both instances the Dow Jones generally saw price appreciation over time. In our view, we don’t expect this to change anytime soon. Just like America has compounded over the last 250 years, the best thing an investor can do is to get out of their own way and let the train keep rolling forward.

Disclosure: Indexes shown: S&P 500 Value, S&P 500 Growth, S&P Mid Cap 400, S&P SmallCap 600 Growth, S&P SmallCap 600 Value, ICE BofA High Yield Bond Index ETF, Bar-clay's Aggregate Bond Index, MSCI World Index ex. US, S&P 500 Real Estate, and Morgan Stanley Capital Index Emerging Markets. This is not an official representation of your asset allocation. The percentages shown were calculated manually and could be subject to transcription error. Your official record of your asset allocation is shown on your official statement from Charles Schwab. Past Performance isn’t indicative of future results. *Performance Date as of 06/30/2026.

1. Kelly, Dr. David JP Morgan Guide to the Markets “Returns and Valuations by Sector” Page 16 10 July 2026

2.Shiller Pe Ratio - MULTPL, www.multpl.com/shiller-pe. Accessed 13 July 2026.

3. Kelly, Dr. David JP Morgan Guide to the Markets “Sources of Earnings growth and profit margins” 13 July 2026

4. Big Tech Is Paying for the AI Boom, and Chipmakers Are Cashing in: Chart of the Day, finance.yahoo.com/markets/article/big-tech-is-paying-for-the-ai-boom-and-chipmakers-are-cashing-in-chart-of-the-day-114043038.html. Accessed 13 July 2026.

5. For 80 Years, the President’s Party Has Almost Always Lost House Seats in Midterm Elections, a Pattern That Makes the 2026 Congressional Outlook Clear, theconversation.com/for-80-years-the-presidents-party-has-almost-always-lost-house-seats-in-midterm-elections-a-pattern-that-makes-the-2026-congressional-outlook-clear-271605. Accessed 13 July 2026.

This commentary on this newsletter reflects the personal opinions, viewpoints and analyses of the Delta Wealth Solutions, LLC employees providing such comments, and should not be regarded as a description of advisory services provided by Delta Wealth Solutions, LLC or performance returns of any Delta Wealth Solutions, LLC Investments client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this website/newsletter constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Delta Wealth Solutions, LLC manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results. Delta Wealth Solutions, LLC a Registered Investment Adviser. This newsletter is solely for informational purposes. Advisory services are only offered to clients or prospective clients where Delta Wealth Solutions, LLC and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Delta Wealth Solutions, LLC unless a client service agreement is in place.

The hypothetical information provided is back-tested performance, was compiled after the end of the period described and does not represent decisions made by Delta Wealth Solutions, LLC.

Specific note concerning graphs, images, charts, formulas, or any other visuals: Delta Wealth Solutions, LLC provides such exhibits for informational purposes only and the data provided alone should not be considered investment advice and should not in and of itself be used to determine which securities to buy or sell, or when to buy or sell them. Any graph, image, chart, formula, or visual should be only be considered in its specific context within this newsletter and from the original source where it is derived. Any use of a graph, image, chart, formula, or other visual is not a solicitation to buy or sell securities in any manner. Any investments should be considered thoroughly and discussed with the readers Financial Advisor.

This publication has been prepared by Delta Wealth Solutions LLC and may not be reproduced or distributed without the consent of Delta Wealth Solutions LLC. This document is for informational purposes only and is not an offer, or solicitation, to buy , sell or hold any financial product or investment. The analysis contained within this publication should not be considered a recommendation and does not take into account the specific goals, objectives, or needs of any recipient. Past performance is no indication of future results and different assumptions could create results that materially alter from the information conveyed in this publication. The opinions and information conveyed within this publication were procured by sources deemed to be reliable. This report is up to date as of the date and time reported on page 1 of this publication.

More information about Delta Wealth Solutions LLC can be found on our website at www.deltawealthsolutions.com, calling us at 816-810-4467, or e-mailing info@deltawealthsolutions.com. Delta Wealth Solutions is a Registered Investment Advisor in the State of Missouri.